Chinese semiconductors and alternative paths to innovation

Faced with tech restrictions, China is searching for new ways to push ahead on semiconductors. Finding such alternative routes could help China "overtake on the curve," like in other industries.

I wrote an introduction to a fascinating piece on the special role of legacy semiconductors for Sinification, a must-read newsletter by Thomas des Garets Geddes that publishes translations of important Chinese-language articles. We are cross-posting my introduction and the translated piece on High Capacity and Sinification.

Introduction

DeepSeek gave the world a stunning demonstration of how China could work around US-led technology restrictions and find new paths for innovation. In a similar way, China’s auto industry was able to overcome challenges with internal combustion engine technology by innovating in electric vehicles and batteries. With semiconductors today, China is trying to get around technology restrictions using a host of strategies, including open-source RISC-V architecture, older DUV lithography, advanced 3D packaging, and chiplets.

In this insightful commentary, He Pengyu (何鹏宇), a former student of renowned Chinese economist Lu Feng (路风), argues that China’s legacy semiconductor industry can play a special role in driving innovation. US restrictions on China’s semiconductor industry are aimed at limiting China’s progress on advanced semiconductors. Both US and Chinese policy efforts have tended to focus more on these leading-edge segments of the semiconductor industry rather than on so-called mature or legacy chips.

He Pengyu argues that this is a mistake. China should also prioritize the development of its legacy chip industry, which provides critical inputs for a wide range of sectors, including automotive, consumer electronics, and high-tech manufacturing. China can leverage its position as the world’s largest chip market to drive scale and innovation in areas such as chip design and packaging

The history of Japan’s semiconductor industry offers a powerful lesson, He Pengyu explains. In the 1960s and 1970s, the US semiconductor industry was focused on what were leading-edge chips at the time for mainframe computers. Japan was able to leapfrog the US by pursuing a less-used technology called CMOS that offered greater power efficiency and was particularly suited for personal electronics like calculators, which Japan dominated. By the end of the 1980s, Japan controlled over 50% of the global semiconductor market, particularly through its production of CMOS-based DRAM.

{kind=link}

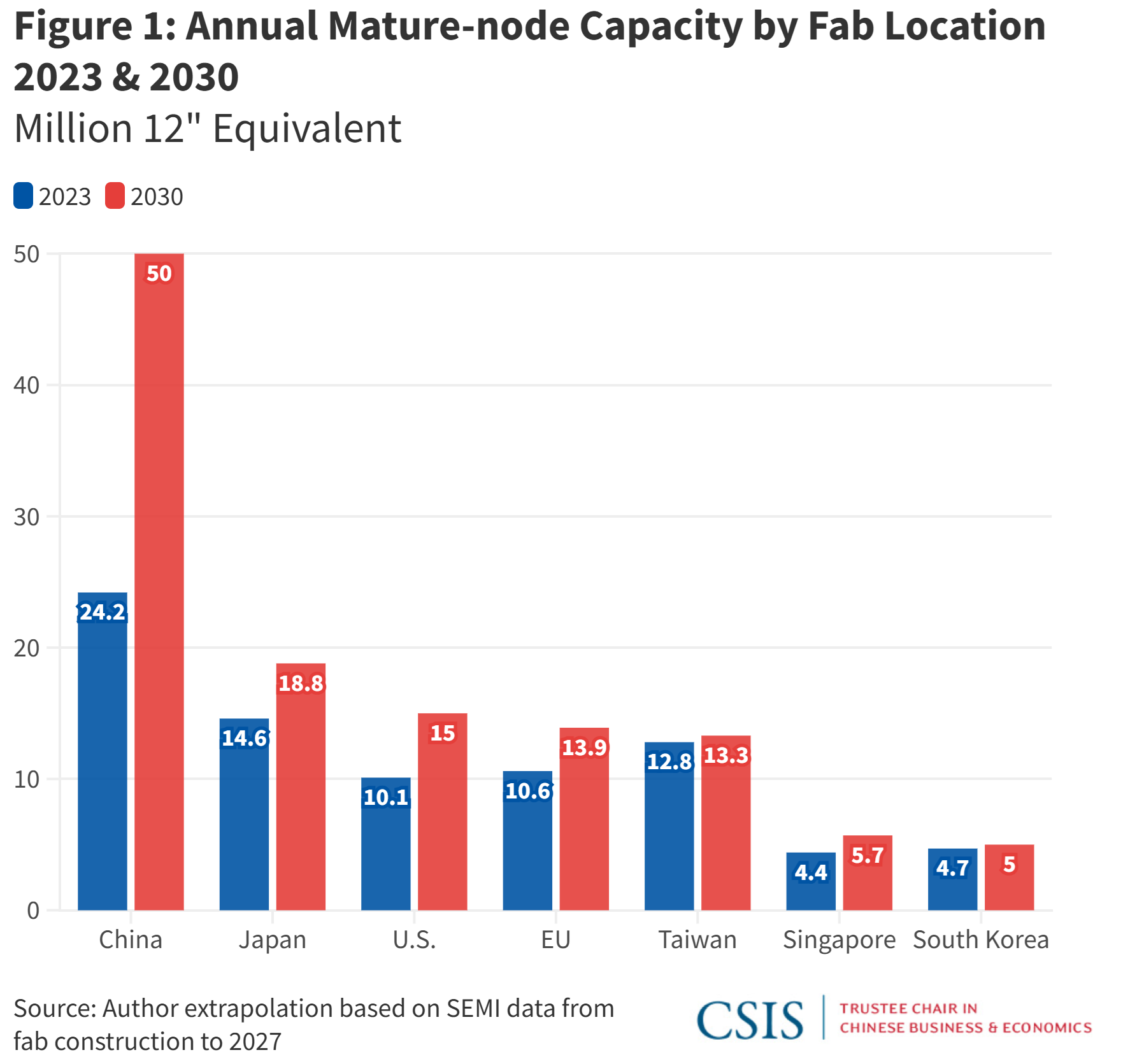

While leading-edge chips dominate the headlines, the US and China have both made efforts to address legacy semiconductors. China has been rapidly expanding its production capacity for legacy chips, which is expected to reach 39% of global capacity by 2027. Chinese chipmakers have already driven down prices for silicon carbide (SiC) chips, which are used for the power and automotive sectors. These trends have made the US and Europe increasingly concerned about possible Chinese overcapacity in legacy chips.

In response, the US is preparing to place tariffs on legacy chips from China, and the US CHIPS Act awarded funding to expand America’s own production of legacy chips. Going forward, He Pengyu argues, China may have the upper hand in legacy chips given its manufacturing dominance in many downstream industries, similar to the way that Japan used its calculator industry to catalyze its semiconductor revolution.

There are broader takeaways from this piece that extend beyond semiconductors. First, traditional industries should not be overlooked in the pursuit of emerging ones, a point made by Zheng Shanjie (郑栅洁), head of China’s National Development and Reform Commission. China’s industrial policy supports both, recognizing that China’s traditional industries help enable its emerging ones.

Second, building up industries that are not necessarily cutting-edge but are large and diverse can provide a useful “training ground” (练兵场) to iterate and innovate. The scale and diversity of China’s legacy chip industry, for example, can drive progress in upstream areas such as chip design and manufacturing as well as downstream applications. Together, these various segments of the chip industry and their application sectors can improve together through a kind of “industrial coevolution.”

Third, innovation can happen along multiple dimensions. There’s a tendency these days to fixate on a single dimension of progress, such as the size of process nodes or scores on LLM benchmarks. But especially for companies or countries playing catch-up, there may be opportunities to leapfrog ahead by discovering entirely new axes of innovation. There’s a great expression that comes from racing: “overtaking on the curve” (弯道超车). When there’s a big shift in the industry, there can be opportunities for players that were previously behind to surge ahead.

- Kyle Chan

IN THE MIDST OF THE U.S. PUBLIC OPINION WAR AGAINST CHINA, CHINA'S CHIP INDUSTRY MUST NOT FALL INTO THE TRAP OF “SELF-SABOTAGE” [自我阉割].

Dr. He Pengyu (何鹏宇) – Postdoctoral Researcher, School of Government, Peking University

Beijing Cultural Review (BCR) – January 2025

With special thanks to BCR and Zhou Anan for granting Sinification permission to share this article.

Translated by by Daniel Crain

Key Points

America’s “Chip War” against China, focusing on restricting access to advanced chips, left a strategic gap for China to rapidly expand its capacity in traditional “mature-process” chips.

Most observers, both in China and abroad, have been seriously underestimating the economic and technological upside of expanding legacy chip-making capacity.

“Traditional” semiconductors account for over 70% of global chip consumption and hold pre-eminence in massive industries like automotive tech and consumer electronics. Dominating this vast market opens up huge revenue flows and opportunities for industrial upgrading.

Historical experience, notably Japan in the 1980s, shows that committing to scale in the chip industry enables latecomers to unlock innovation and productivity breakthroughs.

Although legacy chips may not rely on cutting-edge manufacturing processes, Chinese firms are driving innovation in chip design and advanced packaging, unlocking greater computing power without depending on the latest production technologies.

China should avoid the speculative, venture capital-driven “Silicon Valley model” that prioritizes funding mainly for cutting-edge chips with high profit margins.

Instead, China should favor a strategic approach that emphasizes long-term output growth, cost advantages that attract foreign investment, and sustainable development—paving the way for industrial upgrading and market leadership.

In response to America’s attempt to apply a “chokehold [卡脖子]” on China’s chip industry, China must not be afraid to implement reciprocal and assertive countermeasures against the U.S.

With self-sufficiency in legacy chip production now approaching, China is well-positioned to take such reciprocal action.

China’s biggest hurdle is no longer technology per se, but its entrenched inferiority complex vis-à-vis the developed West; confidence and strategic clarity will determine whether it surpasses global chip leaders. It is certainly on track to do so.

He Pengyu: “As long as China maintains political independence [独立自主], adheres to a “twin-track approach [两条腿走路]” in its industrial strategy—supporting domestic firms in building a competitive edge in traditional chips while persisting with the independent development of advanced semiconductors—then China’s technological catch-up and the overall rise of its semiconductor industry will be only a matter of time.”

I. Why China Needs to Establish a Competitive Advantage in Traditional Chips

In the face of the tech war initiated by Washington, China's semiconductor industry has not only withstood the [US’s] initial suppression of it but has also made significant strides. Regarding these advancements, current discussions mostly focus on breakthroughs in the field of advanced chips, often overlooking another major development—the rapid expansion of Chinese enterprises in the traditional chip sector. This growth momentum has not only propelled China to become the world’s second-largest chip exporter but also put it on track to becoming the largest chip-manufacturing nation globally. However, as traditional chips are often perceived as technologically outdated and lacking financial profitability, the nature and significance of this progress have not been adequately discussed. It has even been regarded mistakenly as a form of industrial involution [内卷] that leads to overcapacity [Note: The author is using the term involution (内卷) a popular neologism commonly used in China to describe a widespread sense of economic and social stagnation arising from relentless domestic competition].

This article approaches the issue from the perspective of technological progress and industrial development, demonstrating that China's expansion in the traditional chip sector is, in fact, of immense significance. Although traditional chips rely on relatively mature manufacturing processes, they still offer substantial opportunities for technological innovation and far exceed advanced chips in terms of application scale. Therefore, as industry leaders dominate the advanced chip sector, focusing on traditional chip development allows latecomers to cultivate unique competitive capabilities. Historical experience in the global semiconductor industry further confirms that successful latecomers—whether countries or companies—have often grown by expanding continuously in the traditional chip sector.

For China, establishing a competitive advantage in traditional chips is not only a strategic countermeasure against the U.S. chokehold [卡脖子] on [our] advanced chip sector but also a crucial step in developing a domestic industrial chain and advancing independent technological capabilities. Amid renewed maximum pressure from the United States on China’s semiconductor industry, China must not "tie its own hands [自缚手脚]” by restricting the expansion of traditional chip production.

II. The Importance of Developing Traditional Chips for Technological Advancement

The concept of traditional chips has emerged only in recent years, broadly referring to integrated circuits produced using relatively mature manufacturing processes, also known as "mature-process chips [成熟制程芯片]”. Compared with advanced chips, which are manufactured using the latest generation of cutting-edge processes, traditional chips are often regarded as insignificant:

First, traditional chips are not at the forefront of manufacturing processes and are perceived as technologically “backwards [落后].”

Second, the market price of traditional chips is significantly lower than that of advanced chips, making them appear less economically profitable.

As a result, for a long time after the United States launched its tech war, discussions in both China and the U.S. largely overlooked [the importance of] traditional chips.

However, this perception actually underestimates the technological potential and industrial value of traditional chips. Traditional chips are not synonymous with technological backwardness. In fact, while their product forms are relatively stable, they still offer numerous opportunities for technological innovation. From the perspective of the interaction between products and technology, every product can be seen as a system composed of multiple technologies in the form of components or manufacturing processes.

However, a product’s performance characteristics—such as functionality, cost and form—are not determined by any single technology alone. Instead, they depend on the attributes of other technologies and the product architecture that defines how these technologies function together. In the semiconductor industry, chip development and production generally involve three key stages: design, manufacturing and packaging/testing. Manufacturing processes are only one aspect of chip technology, not its entirety. Therefore, even when using mature manufacturing processes, traditional chips still have room for innovation and the application of advanced technologies in the design and packaging/testing stages.

With a fixed process node, improvements in traditional chips can still be achieved by adopting new materials, equipment and even new processing techniques, enhancing both quality and cost-efficiency. In other words, so-called traditional and advanced chips merely possess different technological characteristics and evolutionary paths. At the product level, there is no absolute distinction between "advanced" and “backward”.

More importantly, compared to advanced chips, one unique advantage of traditional chips is their significantly larger and more stable application scale. As an intermediate industrial product, the scale of chip applications largely determines the opportunities for technological progress.

Although certain key technological fields require advanced chips, traditional chips—precisely because of their stable manufacturing processes and lower market prices—are widely used in major economic sectors such as automobiles, consumer electronics and mechanical equipment. Meeting the demand in these industries requires consuming 70% of the global chip production annually. Technological changes in these downstream industrial sectors often create broader market opportunities for advancements in traditional chips. For instance, the trends of smart and electric vehicles in the automotive industry are driving a new wave of technological innovation in traditional chips, particularly through the extensive adoption of third-generation semiconductor materials such as silicon carbide.

Because the industrial value of traditional chips far exceeds their apparent financial value, even industry leaders are unwilling to abandon the traditional chip market entirely. For example, TSMC [台积电], which has almost monopolized the global advanced chip foundry business, still maintains a significant proportion of mature-process manufacturing capacity.

However, traditional chips also represent a weak link that industry leaders find difficult to manage, as there are significant differences between traditional and advanced chips in terms of product characteristics and market demand. Since advanced chips command high market prices but have limited application scope, industry leaders can achieve profitability even with high production costs and relatively small-scale production. By contrast, traditional chips have lower market prices but a vast application scale, requiring low production costs and large-scale manufacturing to remain profitable. If we adopt a concept proposed by American scholars who focus on innovation and view the business system formed by firms around product development and application as a specific "value network [价值网络]”, then a frequently occurring situation is as follows: since the value network reflects users' prioritization of product performance characteristics—such as cost versus performance—and because industry leaders continuously strengthen their capabilities based on the “value network” of advanced chips, they often fail to promptly identify and capitalize on market demands and technological shifts in traditional chips.

Thus, since the advanced chip market is often "locked in [锁定]” by industry leaders, limiting opportunities for new applications, the development of traditional chips offers latecomers a pathway to enhance their competitive capabilities continuously. On one hand, latecomers can redefine chip performance characteristics based on specific downstream application needs, driving technological innovation in chip design, packaging and testing, or in materials used and equipment. This allows them to develop unique technical capabilities that industry leaders lack.

On the other hand, by engaging in market competition centered on low costs and large-scale production, successful latecomers often develop manufacturing capabilities that surpass those of the industry leaders.

III. What the Rise and Fall of Japan’s Semiconductor Industry Can Teach China

In the history of the global semiconductor industry, many successful latecomers have built the foundational capabilities needed to catch up with industry leaders through the development of traditional chips. A classic example of this is Japan.

Although Japan’s semiconductor industry surpassed the United States in the 1980s in the field of advanced memory chips, the technological and manufacturing capabilities that enabled this achievement were initially developed in the traditional consumer electronics chip sector. During the 1960s and 1970s, one of Japan’s most important consumer electronics products was the calculator, but the chips required for these calculators were largely imported from the United States.

However, U.S. semiconductor manufacturers were more focused on advanced chips for mainframe computers and, to some extent, disregarded calculator chips due to their highly competitive market and lower prices. The Japanese calculator companies received chips of inconsistent quality and faced high collaboration costs, which compelled them to start working with domestic semiconductor manufacturers to develop their own chips. As market competition intensified, Japanese calculator companies continuously pressured their suppliers to reduce chip prices, accelerate product iteration and shorten delivery cycles. As a result, Japanese semiconductor firms were gradually “forced” [倒逼] to develop capabilities focused on product yield, cost efficiency and large-scale manufacturing.

During this process, Japanese semiconductor manufacturers also developed a technological path distinct from that of the United States. At the time, most U.S. manufacturers focused primarily on NMOS technology for early memory chip products, rather than the somewhat riskier CMOS technology. However, Japanese manufacturers recognised that the low-power consumption characteristic of CMOS technology could significantly enhance the utility of portable electronic devices. They also understood that the risks and costs associated with adopting this new technology could be offset by expanding market scale. As a result, they began developing and applying CMOS technology in chips for calculators and other consumer electronics. As Japanese firms continued to grow in the traditional chip sector, their continuous improvements in CMOS technology gradually provided a cost advantage over NMOS. Moreover, the vast majority of the technical knowledge in this field became concentrated in the hands of Japanese manufacturers rather than American firms.

Eventually, when Japanese semiconductor manufacturers made a major entry into the memory chip sector, U.S. firms were surprised to find that their Japanese counterparts could offer higher-quality chips at prices far lower than what they could sustain.

At first, Americans suspected that the Japanese were engaging in unfair dumping practices, but later evidence proved otherwise. Japanese wafer fabrication plants had not only achieved automated mass production but also significantly outperformed U.S. manufacturers in production yield. This allowed Japanese firms to continuously expand production while fully leveraging economies of scale to reduce manufacturing costs. As a result, when global semiconductor demand surged in 1983 and 1984, Japanese firms were able to expand production swiftly and improve their products to meet customer needs, whereas U.S. firms could only watch as they lost market share. At the same time, as transistor density in memory chips continued to increase, the low-power advantage of CMOS technology became more evident over NMOS. This enabled Japanese firms to accelerate product iteration, while U.S. firms faced repeated setbacks.

Faced with the dual blow of losing both market dominance and technological advantages, the U.S. semiconductor industry fell into an unprecedented crisis in the mid-1980s, ultimately leading to the near-total withdrawal of American companies from the memory chip sector. By 1986, Japanese firms had secured absolute dominance in the global memory chip market.

Japan had successfully surpassed the United States, emerging as the world’s largest semiconductor-producing country.

Ironically, after entering the 1990s, Japan's semiconductor industry suddenly fell into a near 20-year decline. The reasons behind this shift are complex, but overall, Japan’s semiconductor industry took a path opposite to the one that had led to its rise—focusing excessively on technological advancement while neglecting the rapidly changing external market demand—particularly developments in the traditional chip sector. As South Korea, Taiwan and even European countries made significant strides in consumer electronics, industrial electronics, automotive electronics and chips for personal computing and mobile communication devices, Japan’s semiconductor industry failed to respond in time. This ultimately led to a continuous decline in its global market share and a steady contraction of its industrial supply chain.

Regardless, the historical experience of latecomers proves a fundamental principle: the strategic essence of developing traditional chips lies in establishing a foundation of [self-reliant] capabilities despite technological backwardness. Thus, as China faces a “chokehold [卡脖子]” from the United States in the sector of advanced chips, the development of traditional chips offers a crucial pathway for the technological advancement of China's semiconductor industry: By using traditional chips as a “base [根据地]”, China can cultivate unique competitive capabilities—whether in cost efficiency, economies of scale or distinctive technological advancements—which in turn provide the necessary foundation for advancing into the high-end chip sector.

IV. The Strategic Significance of China “Dominating” [主导] Traditional Chips

For China, establishing a competitive advantage in the traditional chip sector is not only justified from a technological perspective but also holds significant strategic importance. To understand this, it is necessary to examine the evolution of the semiconductor tech war. As previously mentioned, traditional chips are just as crucial as advanced chips for economic growth and industrial development. This raises a key question: Why did the United States not seek to completely suppress China’s semiconductor industry from the outset but instead focused its efforts on a “chokehold [卡脖子]” over advanced chips?

In hindsight, the root cause lies in the global supply and demand structure of the semiconductor industry at the time. From the supply side, Chinese companies held an extremely limited market share in the traditional chip sector. In 2020, Chinese domestic enterprises (headquartered in mainland China) accounted for only 5% of global chip production. Although U.S. companies did not produce a large number of traditional chips either, the vast majority of the global market share was controlled by U.S. allies. Meanwhile, companies from the United States, Europe and Japan almost monopolised the global semiconductor equipment and materials market for years. As a result, China’s traditional chip industry was of little concern [不足挂齿] to the United States at that time.

On the demand side, China has been the world's largest single semiconductor market since 2005 and, since 2020, it has been the world's largest semiconductor equipment market and the second-largest semiconductor materials market. The semiconductor companies of the US and its allies depend heavily on China's massive demand, and their innovation and technological advancements also rely on applications in the Chinese market. Thus, if China’s semiconductor industry were completely crushed, the U.S. semiconductor industry would also suffer severe consequences—investment cuts, layoffs, plummeting stock prices and subsequent panic on Wall Street. These effects had already begun to surface in the early stages of the tech war. This is one of the main reasons why U.S. semiconductor companies initially expressed strong dissatisfaction with the U.S. government's aggressive policies.

As the tech war evolved and compromises were made between Washington and [American] companies, the United States gradually adopted a strategy aimed at "having its cake and eating it too [鱼和熊掌兼得]”. On one hand, it imposed a "chokehold" on the advanced chip sector, using export controls and market restrictions to suppress Chinese companies. On the other, it left an "open door [开口子]” in the traditional chip sector, allowing U.S. and allied companies to continue dominating the Chinese market. As a result, while China’s semiconductor industry was cut off from importing critical advanced technologies and equipment, all companies complying with U.S. government sanctions were simultaneously striving to expand their market share in China for traditional chips, related equipment and software.

For instance, around 2020, as U.S. export controls hindered the expansion of Chinese chip foundries, companies such as TSMC, Samsung and UMC actively planned to build or expand mature-process manufacturing capacities in China. Dutch lithography equipment manufacturer ASML decided to expand and upgrade its technical service base in China, aiming to scale up its business in low-end lithography machines. Meanwhile, the world's top three Electronic Design Automation (EDA) software companies continued to occupy a significant share of the Chinese market.

However, these very markets were essential for the growth of China’s semiconductor industry—without market demand, technological advancements could not be refined through application and companies would not be able to sustain large investments in research and development.

It is not difficult to imagine that if the industrial landscape at the time had remained unchanged, every segment of China’s semiconductor industry would have continued to be dominated by international firms, and the outcome of the tech war would probably have been a decisive victory for the United States.

However, by 2020–2021, amid the global disruptions caused by the pandemic and the rise of China’s electric vehicle industry, the semiconductor industry experienced a large-scale chip shortage, with the most significant capacity gap occurring in [the sector of] traditional chips. Faced with this unexpectedly massive surge in market demand, Chinese domestic firms seized the opportunity to expand production rapidly in the traditional chip sector. In 2021 alone, China’s chip production increased by nearly 40% compared with the previous year. Although the global semiconductor market shifted rapidly from shortage to oversupply in the second half of 2022, Chinese domestic firms did not slow their pace of expansion. In 2023, China’s chip manufacturing capacity continued its rapid expansion, growing at a wildly fast [狂飙] rate of 12%, more than twice the global average, and this momentum persisted into 2024. Some research institutes have already indicated that if this growth rate is maintained, China’s chip manufacturing capacity will reach parity with the leading countries by 2025 and surpass them by 2026, making it the world’s largest chip-producing nation.

It is worth noting that despite experiencing intense price competition in 2023, [China’s] leading domestic firms driving expansion have not only continued to see simultaneous growth in revenue and profit but have also maintained high capacity utilisation rates. For instance, in the third quarter of 2024, SMIC’s revenue had doubled compared with the same period in 2020, with net profit increasing by more than 56% and a capacity utilisation rate exceeding 90%. Similarly, Hua Hong Semiconductor [华虹半导体] (a listed subsidiary of Hua Hong Group [华虹集团]) saw its third-quarter 2024 revenue double compared with the same period in 2020, achieving a dramatic turnaround from losses to profitability compared with the previous year, with a capacity utilization rate reaching 105.3%. Meanwhile, in the first three quarters of 2024, Nexchip’s [晶合集成] revenue increased by more than 35% year-on-year, while its net profit surged by 771%.

These three companies (including Hua Hong Group’s overall capacity) have already entered the ranks of the world’s top ten wafer foundries and continue to improve their manufacturing processes. This clearly demonstrates that the expansion of traditional chip manufacturing is built upon sustained growth in production capabilities [制造能力持续成长], rather than the so-called “involution competition [内卷竞争]" within the industry. If there is any claim that China’s approach has led to “overcapacity”, then the excess production should be attributed not to these newly added, highly competitive capacities, but rather to outdated and less efficient manufacturing capacities that are lagging behind.

In addition, the expansion of traditional chip production has also driven unprecedented growth in China's domestic semiconductor equipment, materials and EDA industries. Because the Chinese market had long been dominated by foreign chip manufacturers, Chinese domestic companies in the semiconductor supply chain—including equipment, materials and EDA tools—had also been relegated to the margins, with local market shares typically at or below 10%. Although the semiconductor tech war led to a consensus within [our] industry on the necessity of domestic alternatives in these upstream sectors, replacing foreign suppliers in existing production lines carried significant technological risks and costs. It also required certification from chip customers, which initially hindered the progress of domestic substitution during the first few years.

Against this backdrop, whether aiming to accelerate production and capture market share or in order to avoid the risk of additional U.S. sanctions, Chinese companies significantly increased the proportion of their procurement from domestic suppliers during this expansion process, creating critical space for market growth.

In the equipment sector, China's largest company, Naura Technology Group [北方华创], has experienced rapid revenue growth of 50% annually since 2020. By the first three quarters of 2024, its revenue had already matched its total for 2023—nearly ten times its 2017 level. In the materials sector, semiconductor silicon wafer companies such as ESWIN [奕斯伟] and Shanghai Xinsheng Semiconductor Technology [新昇] have also expanded their production capacity. ESWIN, in particular, has increased its share of global 12-inch semiconductor wafer production to 7%, whereas before 2020, China had yet to achieve large-scale production of this product. In the EDA sector, China’s largest firm, Empyrean Technology [华大九天], saw its revenue exceed 1 billion RMB for the first time in 2023, a fourfold increase from 2019.

Supported by surging revenues, these domestic companies have continuously increased their investment in research and development while expanding their product lines. As a result, the growth of domestic equipment, materials and EDA firms has also provided strong support for breakthroughs in advanced chips.

As a result, China’s semiconductor industry has undergone a major structural transformation. Domestic companies, who had previously each “gone their own way [各自为战]”, operating in isolation across different industry segments, have now begun to establish strong supply-demand linkages, forming the foundation of a domestic industrial chain that supports independent technological progress.

However, such changes will not result in [China’s] "decoupling from the global semiconductor ecosystem [与全球产业生态脱钩]” that some fear. On the contrary, it is encouraging international companies to engage more proactively with China’s upstream and downstream firms. The difference now is that these [international companies] must adopt a more equal footing in these partnerships—otherwise, their Chinese counterparts may outcompete and push them out of the Chinese market.

A recent example is the European semiconductor giant STMicroelectronics (ST) announcing its partnership with Hua Hong Semiconductor to produce 40-nanometer MCU chips in China. The statement from STMicro’s CEO [Jean-Marc Chery] provides the clearest explanation for this decision:

"If we give up our market (share) in China to another company working in the field of industrial or in the field of automotive, the Chinese players, they will dominate their market … And their domestic market is so huge, it will be a fantastic platform for them to compete in other countries.”

The best way to "strengthen international cooperation [加强国际合作]" is now self-evident.

The United States has clearly recognized the transformation of China’s semiconductor industry. In response, its new round of export controls, implemented at the end of 2024, significantly expanded both the scope and intensity of restrictions on Chinese companies. Moreover, it explicitly stated that "weakening China’s domestic semiconductor ecosystem [削弱中国本土半导体生态系统]” was a core objective [Note: no link was available for this quote]. China’s response, in turn, became more assertive than ever before.

Not only did China’s Ministry of Commerce announce a ban on the export of dual-use items to U.S. military users or for military applications, but major industry groups—including the Internet Society of China [中国互联网协会], the China Semiconductor Industry Association [中国半导体行业协会], the China Association of Automobile Manufacturers [中国汽车工业协会], and the China Association of Communications Enterprises [中国通信企业协会] —jointly declared that "U.S. chip products are no longer reliable or secure [美国芯片产品不再可靠,不再安全]”, urging Chinese companies to "carefully consider purchasing American chips [审慎选择采购美国芯片]].”

One of the key reasons China was able to respond so “forcefully” lies in its [recent] ability to produce, at scale, the traditional chips essential to its industries, which has significantly reduced its dependence on imported semiconductors.

As a result, China’s rapid expansion in the traditional chip sector has been a “game-changer” [最大“变数”] since the outbreak of the tech war. If this expansion trend continues, China will gain strategic autonomy in technological development.

Since the U.S. has imposed a "chokehold" on advanced chips, China could likewise apply a “chokehold” on traditional chips as a strategic countermeasure [中国也可以对等在传统芯片“卡脖子”,形成战略反制]. China can also continue to develop and strengthen its domestic [chip] supply chain [做大本土产业链], keeping traditional chips as its foundation.. The immense demand in China’s domestic market will provide Chinese companies with greater investment capacity and more application opportunities than the U.S., thereby enabling China to achieve technological advancements at a faster pace and ultimately surpass the United States.

V. What Does China Still Need to Do?

At present, China has all the necessary conditions to establish a competitive advantage [over other countries] in traditional chips. After more than 70 years of development, China’s semiconductor industry not only has domestic enterprises participating in every major segment of the market, but these companies, driven by the expansion of traditional chip production, are also in the process of forming a comprehensive domestic supply chain. China possesses the world’s largest and most comprehensive industrial system, which not only generates the highest semiconductor demand globally but also ensures a complete supply of essential production resources such as equipment, materials and design software. Furthermore, China has built the world’s largest STEM (science, technology, engineering and mathematics) education system, providing an abundant supply of skilled scientific and technological talent for the semiconductor industry. Maintaining and further strengthening these advantages is undoubtedly a prerequisite for sustaining the growth momentum of China’s semiconductor industry.

However, whether these advantages can be fully leveraged still depends on whether China's semiconductor industry can continue its expansion—especially given that the growth of traditional chips is bound to provoke even greater containment efforts [by the US and its allies].

At such a critical juncture in history, the greatest obstacle hindering latecomers is often no longer objective conditions, but rather their strategic judgment and choices—whether they believe [China’s semiconductor] development has reached its limit [到头], or whether they believe that ‘[leading foreign firms] can be overtaken and replaced’ [彼可取而代也]?

One of the key reasons for the rapid decline of Japan’s semiconductor industry in the 1990s was the government’s strategic decision to retreat. In response to a trade war initiated by the United States in the mid-1980s, the Japanese government signed two unequal "semiconductor agreements”. These agreements not only mandated that foreign chips account for at least 20% of the Japanese market but even imposed price restrictions on Japanese chips, prohibiting them from competing using low-cost [strategies].

While the U.S. imposed heavy tariffs on Japanese chips, Japan was not allowed to impose reciprocal tariffs on U.S. chips. Subsequently, as the U.S. semiconductor industry began to recover and South Korea and Taiwan—supported by the U.S.—entered the memory chip and foundry manufacturing sectors, Japan’s semiconductor industry, "tied its own hands together [自缚手脚]’. [This manifested in] an overemphasis on extreme cutting-edge technologies and niche expertise.

However, once market dominance was lost, even the most advanced technologies were bound to be caught up with eventually. As a result, Japan first lost its dominance in memory chips, then in consumer chips and manufacturing, and ultimately had to retreat to the niche sectors of semiconductor equipment and materials—areas that, even today, are not entirely safe from competition. Of course, Japan's deep political and military dependence on the U.S. left it with few alternatives, but this case still serves as clear evidence that a strategic retreat inevitably leads to failure.

In reality, domestic skepticism [负面评价] in China surrounding the development of traditional chips reflects a [deeply ingrained] social mindset shaped by prolonged technological backwardness. This mindset manifests itself in the long-standing "follower model [跟随模式]” of China's semiconductor industry—one that treats the technological standards and development paths of [foreign] industry leaders as the only correct approach while continuously doubting the feasibility of independent [innovation and] development.

Under this logic, the expansion of international firms is seen as fair market competition, whereas the expansion of Chinese firms is dismissed as disruptive “involution [内卷]”. The U.S. banning its companies from purchasing Chinese-made chips is considered unfair, and thus China should refrain from regulating its domestic market [in a similar manner]. Some even [expect China] to open up its market unconditionally.

The U.S. accuses Chinese semiconductor firms of stealing technology and talent from Silicon Valley, implying that China's rise is inherently illegitimate—yet few recognize that the U.S. once used the same tactics against Japan in the past.

In reality, the semiconductor investment frenzy that emerged in China around 2020 was also a product of the "follower model [随模式]”. In response to the aggressive supply chain restrictions imposed by the United States, China's initial focus was not on strengthening domestic firms through product development and market expansion. Instead, there was a widespread attempt to mimic the so-called "Silicon Valley model [硅谷模式]”, relying on venture capital investment in new technologies and products in the hope of achieving a "shortcut to success [弯道超车]”. The prevailing mindset was that whatever the U.S. had, China should invest in it [美国有什么,中国就要投资什么].

However, technological progress in the semiconductor industry has never been something that can be achieved solely through investment and financing. Instead, capital must be continuously funneled into the long-term process of product development and refinement, with profitability driven by market competition.

As China shifted its focus toward the sustained expansion of its domestic semiconductor industry, the speculative investment wave quickly dissipated. Financial capital that had entered the industry had no choice but to transition into long-term industrial capital, supporting enterprises in product development and market expansion—otherwise, it would have been impossible to exit the market unscathed.

Against this historical backdrop, whether China can maintain firm policy and strategic resolve will fundamentally determine the future of its semiconductor industry. China has no obligation to submit to U.S. interests and must not "tie its own hands [自缚手脚]”:

First, China must not impose self-restrictions on the expansion of its traditional chip production. Instead, it should pursue market dominance as a strategic objective, firmly supporting the continuous expansion of its domestic supply chain and its integration into the global market. The so-called "upper limit [上限]” of traditional chip development should be determined by market competition, not artificial constraints.

Second, given that the U.S. has effectively barred Chinese chips from its market, China must be bold enough to implement reciprocal measures in its own market, preventing American companies that support these restrictions from squeezing out Chinese firms [挤压本土企业的市场空间].

As long as China maintains political independence [独立自主], adheres to a “twin-track approach [两条腿走路]” in its industrial strategy—supporting domestic firms in building a competitive edge in traditional chips while persisting with the independent development of advanced semiconductors—then China’s technological catch-up and the overall rise of its semiconductor industry will be only a matter of time.

| A guest post by

|

| A guest post by

|

Very informative study. Thanks so much!

great reading!