China is trying to reshape global supply chains

China is using "industrial diplomacy" and technology controls to create new China-friendly global production networks centered around China.

Chinese companies are racing to build factories around the world and forge new global supply chains, driven by a desire to circumvent tariffs and secure access to markets. Chinese companies have been building manufacturing plants directly in large target markets, such as the EU and Brazil. And they’ve been building plants in “connector countries” like Mexico and Vietnam that provide access to developed markets through trade agreements. Morocco, for example, has emerged as a surprisingly popular destination for Chinese investment tied to EV and battery manufacturing due to its trade agreements with both the US and the EU.

While tariffs and trade relations may change over time, an expanding global production network creates more robust channels of market access for Chinese companies, particularly as local jobs become attached to Chinese factories. One might see this as the third phase of China’s development of global supply chains more generally. The first phase was about securing access to resources. The second phase—the Belt and Road Initiative—was about building the infrastructure for global production and shipping. And now the third phase is about securing access to markets.

“Industrial diplomacy”

While tariffs and market access are motivating Chinese firms to build new plants abroad, how they’re going about this is not driven by economic interests alone. Beijing is trying to shape the global expansion of Chinese manufacturers, including which countries they invest in and how. Beijing is encouraging Chinese companies to build plants in “friendly” countries while discouraging them from investing in others in a kind of “industrial diplomacy.”

Countries across the developed world and the Global South alike are eager for Chinese companies to build factories in their markets, with the promise of new jobs and new technology. Given its attractiveness, Chinese manufacturing investment can be used by Beijing as a geopolitical tool to reward certain countries and punish others.

At the same time, China has sought to ensure its own centrality in these new China-friendly global supply chains by limiting the export of key technology, including for batteries, EVs, rare earths processing, and lithium extraction. This is a reversal of China’s standard practice of leveraging access to its market to acquire technology from other countries. China’s reluctance to share certain technologies can cause problems with partner countries and has already emerged as a concern with Chinese EV investments in the EU.

Steering Chinese investment

We can see China’s efforts to steer manufacturing investment in a number of places.

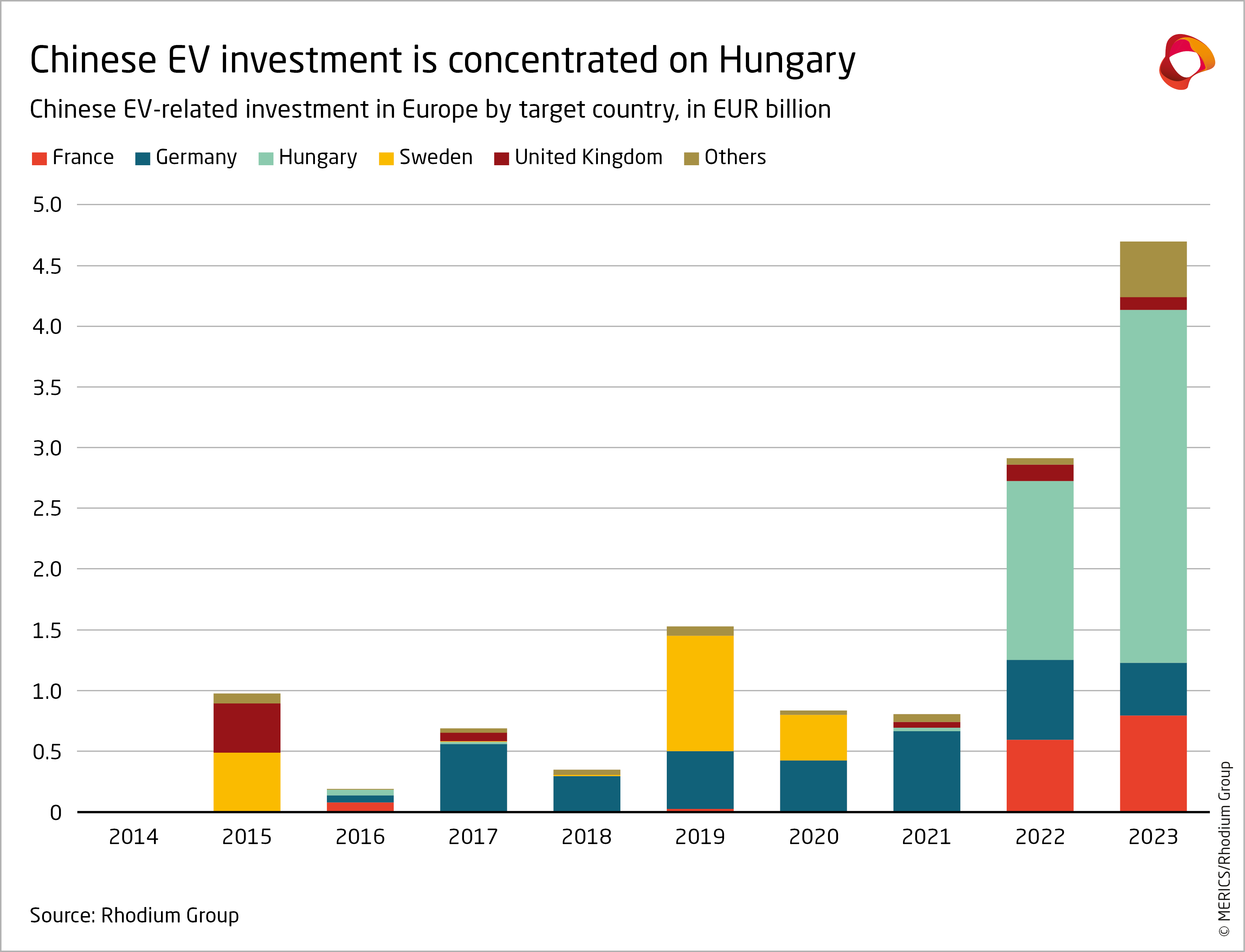

In Europe, China’s Ministry of Commerce has told Chinese automakers like BYD, SAIC, and Geely to pause investments in EU countries that voted in favor of tariffs on Chinese EVs and increase investments in EU countries that voted against them. Chinese firms are prioritizing their EV and battery investments in EU countries that are more friendly to China. Hungary stands out as the largest recipient of Chinese FDI in Europe by far, including a massive $7 billion, 100 GWh CATL battery plant and a new BYD plant slated to start production this year. After Spain abstained from voting on Chinese EV tariffs—seen as a positive move by Beijing—CATL signed a $4.3 billion deal with Stellantis to build a battery plant in Spain.

Brazil, by far the largest recipient of Chinese FDI in Latin America, is another country where warm relations with Beijing have been rewarded with new Chinese factories. Brazil’s President Lula has sought to partner with China to reindustrialize Brazil’s economy and create new manufacturing jobs. BYD and Great Wall Motor are both building EV factories in Brazil after taking over former auto plants from Ford and Mercedes. (Other countries close to China have gotten BYD plants despite a less clear economic rationale, including Pakistan, Cambodia, and Uzbekistan.) Brazil’s rising tariffs on all imported EVs have helped to spur Chinese EV makers to localize production without antagonizing Beijing, unlike the EU which is specifically targeting EV imports from China.

In contrast, the Philippines is a country where Chinese firms have been wary of investing, in part due to tensions in the South China Sea. For years, the Philippines has received only a fraction of the levels of Chinese FDI that its Southeast Asian peers like Thailand and Indonesia have received. The situation worsened even further after President Ferdinand Marcos Jr., known for his more confrontational stance toward China, took office in 2022. Since then, many Chinese infrastructure projects stopped and investment from Chinese state-owned enterprises dried up.

Cutting out India

India represents the most striking case of Beijing’s effort to shape the international behavior of Chinese firms. After a series of violent border clashes culminating in 2020-2021, India clamped down on investment from China. Now across a number of industries, Beijing seems to be discouraging Chinese firms making future plans to invest in India while also limiting the flow of workers and equipment.

Electronics. Recently, Beijing appears to be limiting Apple’s manufacturing partner Foxconn from bringing Chinese equipment and Chinese workers to India. Some of Foxconn’s Chinese workers in India were even told to return to China. This informal Chinese ban extends to other electronics firms working in India but notably does not seem to affect countries in the Middle East or Southeast Asia.

Automotive. Beijing has told Chinese automakers specifically not to invest in India. India has been increasing scrutiny of Chinese automotive investment, blocking a 2023 plan by BYD to set up a plant in Hyderabad on national security grounds and putting pressure on SAIC’s MG brand.

Solar equipment. China has been reportedly blocking the export of Chinese solar equipment to India. India’s solar industry relies heavily on China for inputs, including for 80% of India’s solar cells and modules, as well as manufacturing equipment.

Tunnel boring machines. TBMs made in China by Germany’s Herrenknecht for export to India have been reportedly held up by Chinese customs. Analysis by the Takshashila Institution shows that while India does import some TBMs from China, the scale is not large enough to have a meaningful impact.

India is not only a geopolitical rival to China but also a potential manufacturing threat. India is making a huge manufacturing push and has gotten a significant boost from multinational corporations seeking to diversify their production away from China. Apple went from making just 1% of iPhones in India in 2021 to an incredible 14% in 2024, including its most premium model, the iPhone 16 Pro. The stunning speed with which India has been able to ramp up iPhone production and develop its electronics manufacturing industry likely shocked Chinese policymakers and helped spur efforts to slow down India’s progress.

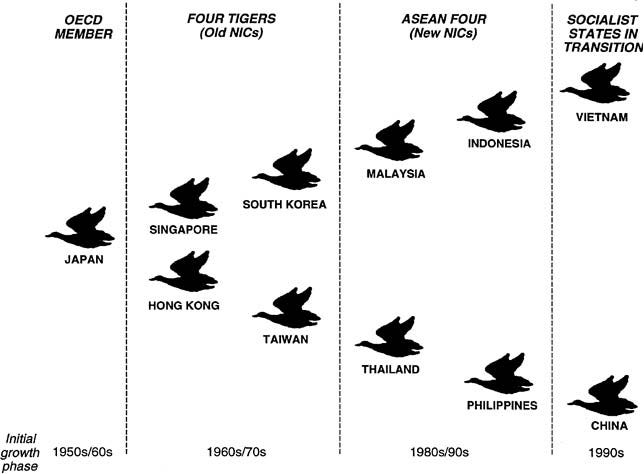

Japan, South Korea, and Flying Geese

In some ways, China is following in the footsteps of Japan and South Korea, which moved production to other parts of Asia as they became more developed. In the process, each country supports the industrial development of the next cohort of countries in a “flying geese” pattern.

Japanese and South Korean firms built supply chains across Southeast Asia to lower production costs and reach Western markets. Samsung invested heavily in manufacturing plants in Vietnam. Japanese automakers like Toyota, Honda, and Nissan set up auto plants across Thailand, Malaysia, Indonesia, and the Philippines. Japanese and Korean chipmakers helped turn Malaysia into a top semiconductor producer.

And of course, Japan and South Korea helped turn China into a global manufacturing hub.1 Along the way, Japanese and Korean companies frequently brought over their own machinery and equipment while keeping the high-tech, high-value work at home.2

Japanese and Korean firms also invested in manufacturing plants to access protected markets and relieve trade tensions, particularly with the US. Japanese and Korean car companies set up auto plants in major markets like the US, Europe, Brazil, and India. Japan’s Daikin set up air conditioning factories in Mexico and India. Korea’s LG made home appliances in Brazil and Europe. Now a wave of Japanese and Korean battery plants are springing up across the US and EU.

Now as China is forming new global supply chains, it’s building on existing ones established by Japan and South Korea as well as the West. Chinese EV makers can build on Toyota and Nissan’s supply chain in Thailand. Chinese electronics companies can build on Samsung’s manufacturing base in Vietnam.

And, like Japan before it, China is using these economic linkages to support its own national interests while framing them as mutually beneficial partnerships. China is not the only country that loves using the phrase “win-win” when describing international partnerships. Shinzo Abe used it frequently when talking about Japan’s relationship with the US, EU, Russia, Asia, and of course China. For decades, Japan claimed credit for using aid and investment to help its Asian neighbors develop economically while turning the region into Japan’s manufacturing backyard. Throughout this whole process, Japan was careful to maintain control over core technology and prevent technology “leakage” to other countries.3 Now China is doing many of the same things with a similar framing.

But there is one important difference. China appears willing to leverage its control over technology, machinery, and critical inputs to actively undermine the industrial development of other countries—India being the prime example. In a not-so-ironic twist, China’s approach looks more like that of another great power, namely US efforts to cut out China.

Lee, Chung. 1994. “Korea’s Direct Foreign Investment in Southeast Asia.” ASEAN Economic Bulletin.

China was a more attractive destination for Japanese and South Korean manufacturing investment than ASEAN because of its large protected market, lower production costs, and most stable labor environment. See: Kim, Eun Mee and Jai S. Mah. 2006. “Patterns of South Korea’s Foreign Direct Investment Flows into China.” Asian Survey. Also see: Lee, You-Il. 1997. “Korean Direct Investment in Indonesia in the 1990s: Dynamics and Contradictions.” Asian Perspective.

Japan’s MITI and JICA played instrumental roles in shaping Japanese investment and technical cooperation across Asia. At the same time, Japan saw technology as crucial to retaining control. See: Hatch, Walter. 2003. “Japanese Production Networks in Asia: Extending the Status Quo” in William Keller and Richard Samuels (eds.) Crisis and Innovation in Asian Technology.

Wake up babe! Kyle Chan just dropped another banger. Keep up the good work, and thanks for your insightful article.

Good summary.....but you have to be careful in terms of cause and effect. The companies involved are all competing in global industries and making decisions based on their business models, and are not/not being directed to do certain investments from Beijing. Of course Beijing is cautioning Chinese companies on investments in India and steering EV makers toward countries in Europe that opposed tariffs, this is what governments do. The interaction between Chinese government preferences and company business models is the really interesting part of the story here, sometimes they align, often they do not....