Chinese solar and the German paradox

Germany seemed poised to dominate solar. Yet it was Chinese solar firms who used German equipment to make solar cells and modules to sell back to Germany's subsidized market. What happened?

(This piece draws heavily from Gregory Nemet’s book How Solar Became Cheap: A Model for Low-Carbon Innovation and Kelly Sims Gallagher’s book The Globalization of Clean Energy Technology: Lessons from China.)

The German Paradox

Let me describe what I call the “German paradox” (which also applies to other countries): How is it that countries with pioneering technology, early market adoption, sophisticated industrial ecosystems, and abundant capital get overtaken by China in so many industries? In solar manufacturing, Germany at one time seemed to enjoy unbeatable advantages only to later have Chinese firms run circles around them. What happened and what does this say about industrial competition with China more broadly?

Germany’s Supply and Demand Boost

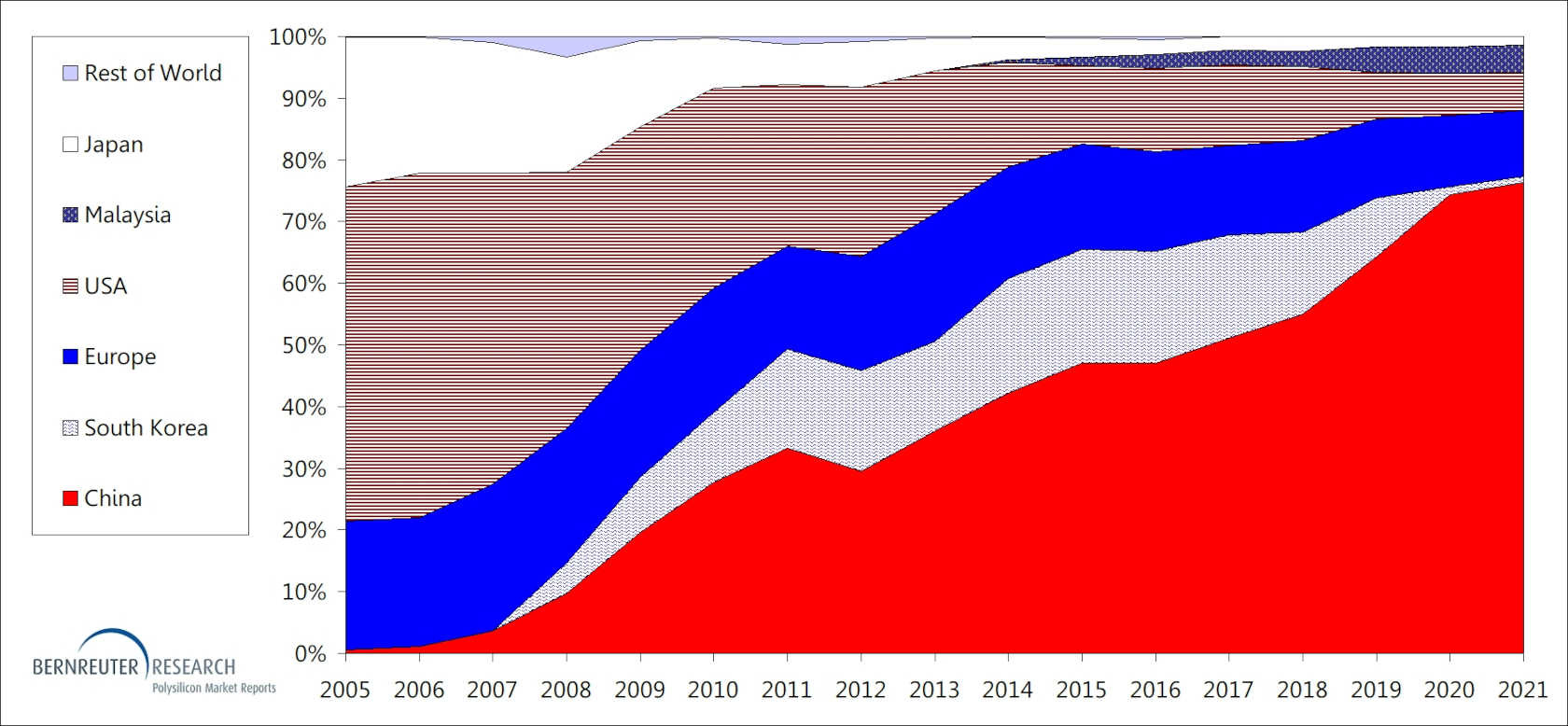

In the 2000s, China’s solar industry was completely transformed by two game-changing developments in Germany. (Other countries were involved too, but Germany’s role looms large.) One was a change in Germany’s renewable energy policy—the Renewable Energy Sources Act (EEG)—that triggered a global surge in demand for solar power. Specifically, Germany established feed-in tariffs, which guaranteed substantial revenues for electricity from renewable sources, such as solar. This caused a boom in demand for solar modules and cells. At its peak, Germany made up half of the world’s new solar installations from 2004 to 2010.1

The other big development around the same time was the rise of “turnkey” solar manufacturing equipment made by German companies. German machinery firms like Centrotherm started selling sets of PV manufacturing equipment as complete all-in-one production lines. German technicians would even set up all the equipment and train your staff how to use them. These turnkey production lines enabled firms without deep expertise in solar technology to quickly jump into PV module and cell manufacturing.

Chinese solar firms quickly put two and two together. They imported turnkey PV production lines from German equipment makers and then sold Chinese-made solar modules and solar cells back to Germany’s booming renewable energy sector. Of course, other countries were in on the game too. The US, Italy, Switzerland, and Japan also made solar manufacturing equipment bought by Chinese firms. And solar manufacturing firms in South Korea and Taiwan also imported similar equipment to build up their manufacturing capacity.

But where were the Germans? With direct access to the biggest market in the world for solar at the time and access to German equipment suppliers, German solar manufacturers seemed poised to dominate the world. Indeed, for a time, German firms like Q-Cells and SolarWorld were the world leaders, taking the crown from Japanese solar makers like Sharp. But, as Gregory Nemet argues, they were never able to scale up as quickly and reduce costs as aggressively as their Chinese competitors. Despite their obvious advantages, German solar manufacturers seemed to have been beaten at their own game by Chinese upstarts.

How did China do it?

Let’s look at some possible explanations.

China’s scientific knowledge base in solar. China’s efforts to develop solar photovoltaic (PV) technology go back to the 1950s and 1960s when Chinese researchers were studying solar power for space satellites (like the US did). China’s R&D efforts on semiconductors also helped position it later for polysilicon production and making solar manufacturing equipment. Yet during the early boom years, the country was short on talent, and Chinese firms had to recruit Chinese PhDs trained at foreign universities, paying them top dollar.2 Germany was in a far better position in terms of both scientific research and industry expertise.

Labor costs. Lower wages did help Chinese solar module manufacturers cheaply turn imported German solar cells into modules, which they sold back to Germany and other markets. But solar cell production has long been highly automated, including in China. The real cost constraint for solar cells was equipment and inputs. Germany had an advantage in both these areas as a producer of manufacturing equipment and a producer of polysilicon, the primary material in solar cells.

Financing and subsidies. China’s central government provided billions of dollars of credit to support the solar industry, particularly through China Development Bank. But this didn’t start until 2009 after Chinese solar firms were already dominating the global market. Instead, Chinese firms relied on two other sources of financing. One was local government support at the provincial or municipal level. For example, the city of Wuxi gave Suntech’s founder financing and support to convince him to move there from Australia (he later thanked Wuxi’s party secretary for his success). While US and German solar firms accused Chinese firms of unfairly benefiting from subsidies, the US and European countries were also providing their own solar industries with subsidies and other support.

The other source of financing was US capital markets. Chinese solar firms like Suntech, Trina, Yingli, Jinko, and JA Solar raised hundreds of millions of dollars listing on the NYSE or Nasdaq. (Many of these stocks later tanked or were delisted when the solar market crashed.)

Solar demand in China. Today, China is by far the single largest market for solar energy, adding more solar capacity in 2023 alone than the US has added in its entire history. But interestingly, China’s surge in solar manufacturing predated its surge in domestic solar power capacity, which really took off with China’s own feed-in tariff program in 2011. So while China’s own renewable energy policies would later help its solar manufacturers survive during a difficult period for the global solar industry, it was really demand outside of China—namely, in Germany and other parts of Europe—that launched China’s solar industry as a global force.

Speed and nimbleness. The speed and scrappiness of Chinese solar firms is emphasized in both Gregory Nemet and Kelly Sims Gallagher’s accounts. Nemet describes how Suntech’s founder Shi Zhengrong flew around the world to cobble together refurbished manufacturing equipment from Germany, Italy, and Japan and get new production lines rolling as quickly as possible.3 Gallagher cites an interview with a foreign manufacturer who said that “the speed at which the Chinese can react to orders and other changes in the marketplace is unrivaled.”4 Germany’s Q-Cells, for a time the world’s largest producer of solar cells, was also able to rapidly scale up in response to Germany’s sudden surge in solar demand. But when prices later fell, Q-Cells had trouble cutting costs as quickly as its Chinese competitors and ended up losing billions of dollars a year until they were eventually bought by South Korean conglomerate Hanwha.

What this means for today

There isn’t a clear answer to the German paradox. One of the best explanations seems to be the relative speed and resourcefulness of Chinese firms, a feature that comes up in many other industries from EVs to smartphones. But this type of explanation is difficult to observe and quantify, leaving us with impressive stories but inconclusive comparisons. Ideally, one would interview people who had worked with both Chinese and German solar manufacturers to understand how differently they operated on the ground.

Now the picture is further muddied by the extent to which Chinese solar firms have solidified their advantages. China has built out a comprehensive solar supply chain, and many Chinese solar firms have gone all-in on vertical integration. Even the solar manufacturing equipment that was once imported from Germany is now mostly made by Chinese companies. One can easily tick off the reasons for China’s continuing dominance in solar today, but the question of what happened in that critical ramping-up phase remains a mystery.

Today we’re witnessing various iterations of the German paradox unfold in real time before our eyes. Chinese EVs and batteries have gone from being mocked for their poor quality and crude design to being feared as a global threat (although they shouldn’t be). And behind these headline-grabbing sectors are dozens of other lower-profile industries where Chinese upstarts have quietly gone from technological laggards to industry leaders: cranes, tunneling machines, bridge-building machines, active pharmaceutical ingredients, petrochemicals, rail infrastructure, and shipbuilding—to name a few.

Yet, there’s a reason I call this the German paradox. The real puzzle is not just why China got ahead but why other countries with a clear head start so often find themselves slipping behind.

More reading:

Gregory Nemet. 2019. How Solar Energy Became Cheap: A Model for Low-Carbon Innovation. Particularly Chapter 6: “German Demand-Pull” and Chapter 7: “Chinese Entrepreneurs.”

Kelly Sims Gallagher. 2014. The Globalization of Clean Energy Technology: Lessons from China. Particularly Chapter 3: “Four Telling Tales.”

See Chapter 6: “German Demand-Pull” in Gregory Nemet. 2019. How Solar Energy Became Cheap: A Model for Low-Carbon Innovation.

See Chapter 7: “Chinese Entrepreneurs” in Gregory Nemet. 2019. How Solar Energy Became Cheap: A Model for Low-Carbon Innovation.

See Chapter 3: “Four Telling Tales” in Kelly Sims Gallagher. 2014. The Globalization of Clean Energy Technology: Lessons from China.

I wonder how much does learning curve play here. At the end of the day, it is a function of demand and especially domestic demand. China now installs nearly half of global solar every single year and the scale is tremendous. And there are many favourable conditions for China the scale up.

Surely cheaper energy costs in China gave them a significant competitive advantage in what is a very energy intensive industry?